Employer of record services in Germany: Legal and tax rules for personnel deployment

10.10.2025

If companies want to hire skilled workers abroad, they can use the employer of record (EOR) model. This allows them to employ skilled workers abroad without having to be registered as an employer in the respective country. Furthermore, the EOR assumes all administrative and legal obligations related to the employment. The Ecovis experts explain how the EOR model works in practice.

The EOR model qualifies as leasing of employees according to German law. In this process an employee is assigned by an employer of record to a client (company) whereby the client has the right to issue instructions. In Germany, leasing of employees is subject to strict regulations under the Employee Leasing Act (in German: AÜG). Among other things, this stipulates statutory permission, a ban on chain hiring, and compliance with certain working conditions.

Whether the AÜG is applied to EOR models depends on the domestic reference. If the leased employee works in Germany or if the EOR is based in Germany, the AÜG applies.

In which cases is the applicability of the AÜG disputed?

There is a controversial discussion about the applicability of the AÜG in cases where the client is based nationally (in Germany) and the EOR is based abroad, while the employee exclusively works abroad. The prevailing opinion negates that sufficient domestic reference is given if solely the client is based in Germany.

What does the Rome I Regulation govern?

The question of applicable law in cross-border employment relationships is governed by the Rome I Regulation (Art. 3, 8 Rom I-VO). As a rule, the working contract is subject to the law of the country in which the employee performs their work or, in exceptional cases, where the EOR has its registered office.

Which advantages does the EOR model offer for companies?

Flexibility: Companies can easily hire professionals abroad without having to register as a foreign employer or establish a subsidiary.

Cost efficiency: The administrative effort for the company is reduced significantly, as the EOR takes on all legal and tax obligations.

Risk minimisation: Companies forego the effort of having to comprehend and apply foreign labour laws and tax regulations.

Risk management: Which aspects should be considered when using an EOR?

Contract design: It is crucial to have detailed and unambiguous contracts between the company, the EOR and, if applicable, with an intermediary. The contracts should define the modalities of leasing of employees and the responsibilities for compliance with foreign laws as well as the cost distribution.

Compliance: Companies must ensure that the EOR is compliant with all local labour laws and tax regulations. It is advisable to check compliance regularly.

Liability risks: Companies should ensure contractually that they are not liable for any violations of foreign labour laws or a lack of permits for leasing of employees.

We advise you on all legal and tax issues relating to the EOR model and temporary employment in Germany Marcus Büscher, Lawyer, Partner, ECOVIS Deutschland, Düsseldorf, Germany

The trend in case law and the plans of the German Federal Government

In recent cases, the German Federal Labour Court (in German: BAG) has confirmed the strict interpretation of the AÜG. For example, it was clarified that in the absence of a permit for leasing of employees, an employment relationship between the client and the employee can be simulated (§ 10 Abs. 1 AÜG). This emphasises the necessity of abiding by legal regulations.

The German Federal Government is planning to facilitate the immigration of professionals, which could further increase the appeal of the EOR model. At the same time, the requirements for leasing of employees may potentially be tightened, which further highlights the importance of careful contract design.

Careful contract design and proactive risk management

The EOR model offers companies a flexible and efficient opportunity to employ professionals abroad. However, this form of employment also includes legal risks, especially regarding the application of the AÜG and compliance with local regulations.

Careful contract design and proactive risk management are therefore essential in order to fully benefit from the advantages of the model and to avoid legal pitfalls.

For further information please contact:

Marcus Büscher, Lawyer, Partner, ECOVIS Deutschland, Düsseldorf, Germany

Email: Marcus.Buescher@ecovis.com

State pre-emption right in the Hungarian M&A market

10.10.2025

The Hungarian state legislature has recently passed a number of laws seeking to give special protection to certain parts of their national economy. For example, with regard to real estate, a so-called “self-identity” law has been introduced, giving municipalities the possibility to make it more difficult or prohibit newcomers from acquiring real estate on the grounds of their interests in the municipality.

With regard to company acquisitions, Government Decree No 561/2022 (XII/23), recently amended on 24 June 2025, has placed the right to exercise the right of first refusal or even to prohibit the transaction at the ministerial level, rather than at the municipal level. The reason given by the legislator for the regulation is the public interest, but this is not specified in detail.

The term of strategic company

These options are available for companies that are classified by law as strategic companies and that are intended to be acquired by a foreign investor. In each case, the definition of a strategic company must be based on the actual activity of the company concerned and whether it falls within one of the strategic business lines.

Interestingly, one of the strategic sectors highlighted by the legislation contains specific provisions for the activity of “Electricity generation from renewable sources”, which mainly concerns companies operating solar power plants.

The foreign investors concerned

The provision divides foreign investors into two main categories. It distinguishes between (i) nationals and legal entities from the European Union, the European Economic Area and the Swiss Confederation and (ii) from outside these territories.

Value of the investment

In some cases, the legislation excludes from the transactions to be examined transactions that are smaller than an investment in terms of the amount of the investment, and for these transactions the applicable limit is e tat HUF 350 million in terms of the total value of the investment.

The examined types of the transactions

It is not only in the context of the sale of shares and business quotes when it is necessary to examine whether a notification to the Ministry is required. Several transactions, including the increase of capital in the company, the transformation, merger or division of a strategic company, the issue of bonds convertible into, subscribable to or exchangeable for shares in a strategic company, and the creation of a beneficial interest in shares or units of a strategic company, are among the transactions to be examined.

The lenghts of the procedure

The Ministry has a basic procedural time limit of 45 days and a 15-day additional period, which may be extended by up to 30 working days on three occasions, of which the affected party will be notified in writing before the expiry of the time limit. This will definitely slow down the acquisition process and make the success of the M&A transaction uncertain for this period, while it may also generate a loss of interest for the buyer.

Practising of the state pre-emption right

On the basis of their examination, the competent Minister, acting on behalf of the Hungarian State, may prohibit the transaction and the Hungarian State, through the Hungarian National Asset Management Limited Company or another designated body, may exercise its pre-emption rights in respect of the company concerned, subject to the conditions set out in the transaction.

Penalty for the missed examination

Failure by the company to complete the necessary procedure could be an obstacle to its acquisition of ownership before the Companies Registry and could result in a significant fine for the companies concerned.

Mandatory legal representation

Legal representation is mandatory in the proceedings before the Ministry, and it is therefore essential to engage a lawyer. If you wish to buy a company in Hungary, please contact our colleague, the author of the article, Dr. György Zalavári, who is the head of the Ecovis Zalavári Legal Hungary office

Tax deductible costs Poland: Changes in tax cost limits for passenger cars

09.10.2025

On 1 January 2026, the current limits relating to expenses associated with the use of passenger cars in business activities, which are classified as tax-deductible costs, will be replaced. The new limits will depend on the level of carbon dioxide (CO2) emissions. The Ecovis experts explain the impact of the new regulations on operating costs.

The new emissions-based limits are the result of an amendment to the Corporate Income Tax Act, which aims to promote low-emission vehicles and support the ecological transformation of company fleets.

Background

Polish tax law commonly applies various limits on amounts relating to, among others, tax deductions, income deductions, one-off depreciation, the obligation to prepare transfer pricing documentation, or VAT settlement purposes. One such limit is the limit on expenses for passenger cars used in business activities, which are classified as tax-deductible costs.

Current limits

Currently, depreciation of passenger cars is not considered tax-deductible for the amount of the value of the car exceeding:

PLN 225,000 (Polish Złoty, PLN 100 = approx. EUR 23) for electric or hydrogen-powered passenger vehicles

PLN 150 000 for other passenger cars

Limits applicable from 1 January 2026

From the new year, the following limits, which are based on the level of CO2 emissions, will apply:

PLN 225,000 for electric or hydrogen-powered passenger vehicles (this limit will remain unchanged)

PLN 150,000 for passenger cars whose CO2 emissions from an internal combustion engine are less than 50 g per kilometre, based on data contained in the central vehicle register

PLN 100,000 for passenger cars whose CO2 emissions from an internal combustion engine are equal to or higher than 50 g per kilometre, based on data contained in the central vehicle register

We'll discuss the impact of the new regulations on your operating costs with you. Contact us. Hubert Kaczyński, Tax Advisor, ECOVIS Poland, Warszawa, Poland

This is what companies should know and consider now

The change will undoubtedly have a practical impact on the costs of running a business. One issue that remains to be resolved is how the change in limits will affect tax-deductible costs related to the use of cars under a lease or rental agreement.

The transitional provisions to the act indicate that the new regulations will apply to cars entered in the fixed asset register from 1 January 2026, replacing the old (more favourable to taxpayers) rules.

The introduction of fixed assets into the register generally means that the car has been purchased by the taxpayer. This can lead to the unfavourable treatment of expenses related to the use of cars under a lease or rental agreement.

The wording of the regulations indicates that the new limit will apply to the settlement of costs of cars used under a lease, rental or hire agreement, even if the agreement was signed before 1 January 2026. This means that the old limit will apply to expenses incurred before 2025, while the new limit will apply to expenses incurred after 2026, which in turn may lead to unequal treatment of taxpayers.

This unfavourable approach to the recognition of costs of cars used under a lease, rental or hire agreement was recently confirmed by the Ministry of Finance.

Blackbox AI: Lack of knowledge more of a concern than data protection

08.10.2025

A recent study by the global partner law firms of ECOVIS International shows that Artificial Intelligence (AI) is still remarkably underutilised in companies – despite clear benefits such as efficiency, cost savings and higher productivity. Why is this? Perhaps it is due to restrictive legislation or fears of personal data misuse?

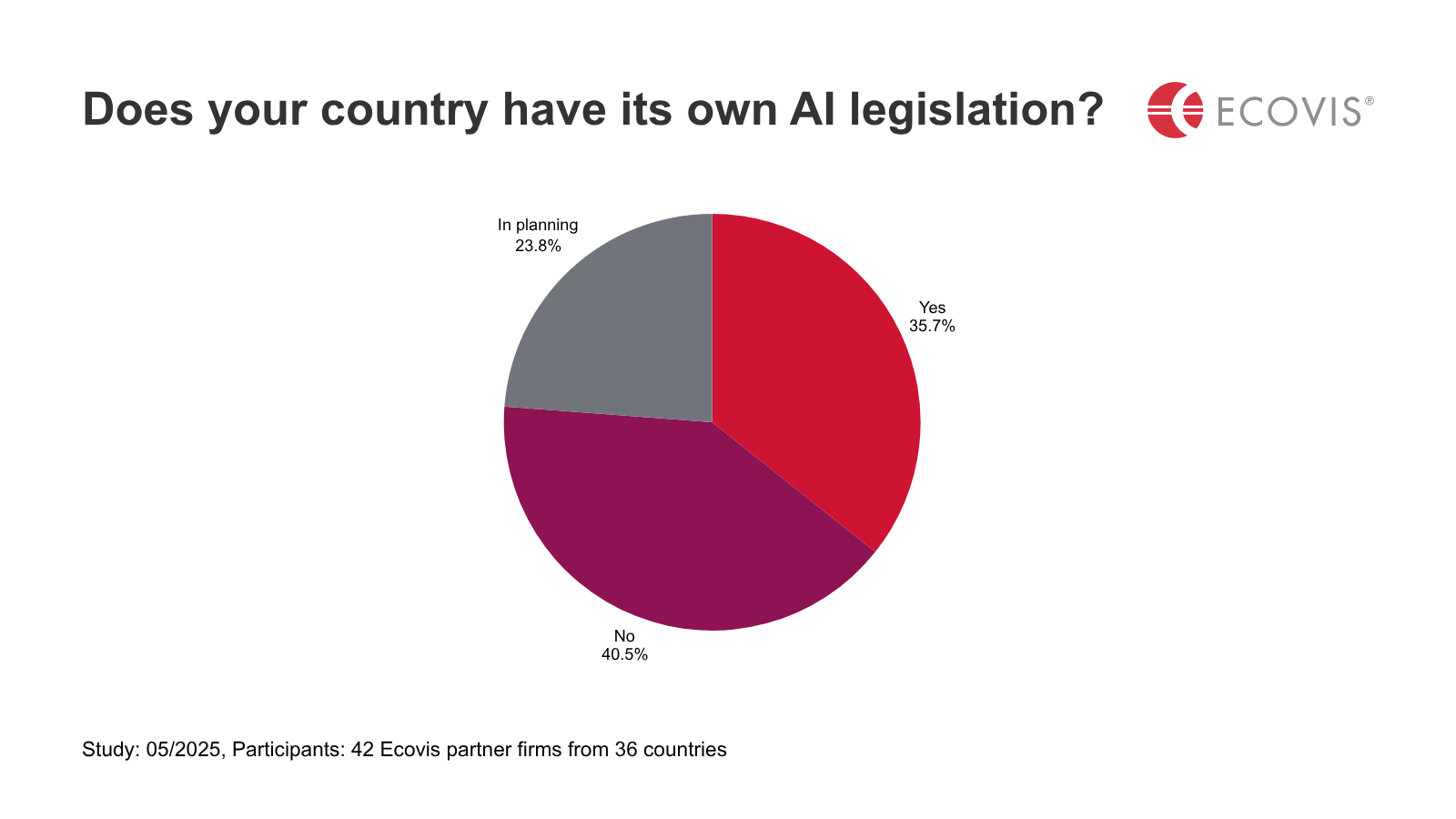

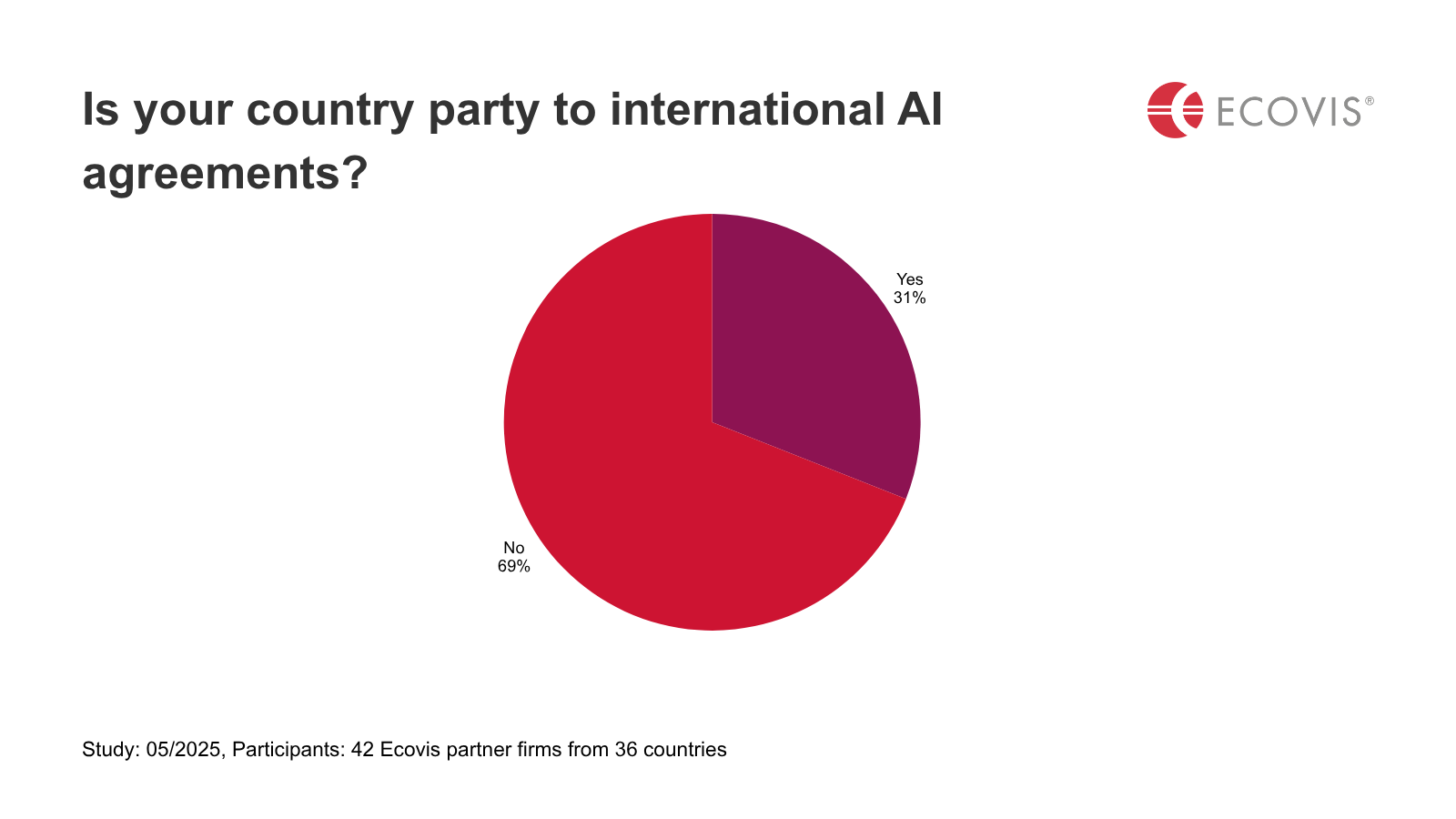

Patchwork AI legislation worldwide: opportunity or risk?

42 law firms from 36 countries took part in the ECOVIS International survey (see below for details). At the time of the survey in May 2025, countries with no legal regulations were still in the lead with 40.5 per cent, while the majority (69 per cent) were party to international agreements.

Uniform legislation in the EU

What is striking here is that uniform legislation is only ensured within the EU with the EU AI Act. It is supplemented in some cases by national regulations that have an impact on the use of AI. There are no cross-border regulations in the Americas, APAC and MEA regions. However, many countries, including Argentina, Brazil, China, Japan, Israel and Mauritius, are part of AI regulations of international organisations such as the OECD and the UN, or are planning their own laws.

National legislation is primarily aimed at protecting against various risks. According to the partner law firms surveyed, these include the protection of fundamental and human rights, the maintenance of public safety and the protection of critical infrastructure, in particular in the healthcare sector.

When it comes to data protection, the EU is playing a pioneering role with its General Data Protection Regulation (GDPR), supplemented by national laws in some member states. Countries such as Brazil, Vietnam, Japan, China,Israel and South Africa also have specific regulations in place. In many countries, however, clear regulations are still lacking or are only just being developed.

Only a few countries have specific laws governing AI violations. These include Japan, China, Spain and the United Kingdom. In all other countries, violations fall under general legislation such as consumer protection, civil law or the GDPR.

“The regional differences are interesting here. Europe, for example, is increasingly aware of the risks and tends to favour stricter regulations. The USA, on the other hand, currently wants to regulate less and thus secure its chance to play a pioneering role in AI,” says Alexander Weigert, Vice President of ECOVIS International.

What exactly does this mean for companies?

It is difficult for international companies to useAI applications across borders. This is because differing legislation on what is permitted in individual countries, as well as restrictions such as data protection, make it difficult for companies to develop a uniform AI strategy or use AI models in the same way in all countries. The exception here is that, thanks to the AI Act, EU Member States have uniform regulations, which makes work easier for international companies – and could be a competitive and locational advantage in the future.

Promoting AI at the expense of personal data protection?

Countries have two main tasks in the development of AI worldwide: funding initiatives and regulatory measures. According to the participating partner law firms, the focus of governments is on promoting innovation while complying with existing laws and regulations.

Amercias region

Among the countries that specifically promote research, development and application of AI in the Americas region, Colombia stands out alongside Brazil: here, the government introduced guidelines in 2019 and 2020 that promote research, the ethical use of AI and an innovation ecosystem. There are also special institutions for financing AI projects. The USA is providing USD 500 billion to build AI infrastructure as part of the Stargate project. In February, Europe launched the InvestAI initiative, which aims to mobilise EUR 2 billion for investment in AI.

APAC region

In the APAC region, there are specific initiatives in Vietnam, China and Taiwan. Japan is particularly noteworthy: on the one hand, it has a USD 65 billion plan to promote the domestic AI industry, among other things, as well as partnerships with US starts-ups to train Japanese engineers in the development of AI chips. Secondly, the Japanese government has proposed amendments to the data protection act to facilitate the use of personal data in AI development. “This is still only a proposal. The extent to which such measures would also be possible in Europe, for example, is questionable. This is because the relaxation of personal data protection is viewed very critically in some quarters here”, says Richard Hoffmann, solicitor and member of the Management Board of ECOVIS International.

EU and United Kingdom

Almost all countries in the EU and the United Kingdom have initiatives to promote AI. Poland, for example, plans to establish a national AI authority, while Portugal already has a national AI agenda aimed at driving technological progress, training specialist workers and expanding the necessary infrastructure. It is also striking that many countries, such as Greece and Latvia, are promoting cooperation between research, industry and the public sector in order to implement innovations in a practical manner. Another key element is financial support, for example through national funding or EU programmes such as Horizon Europe. Italy stands out in this regard, providing targeted funding for small to medium-sized enterprises.

What does that mean in summary?

Even though most of the funding programmes are still in their infancy and results are yet to be seen, the various state funding initiatives show that governments want to harness the potential of AI. Companies should find out how they can meet requirements for funding in their country.

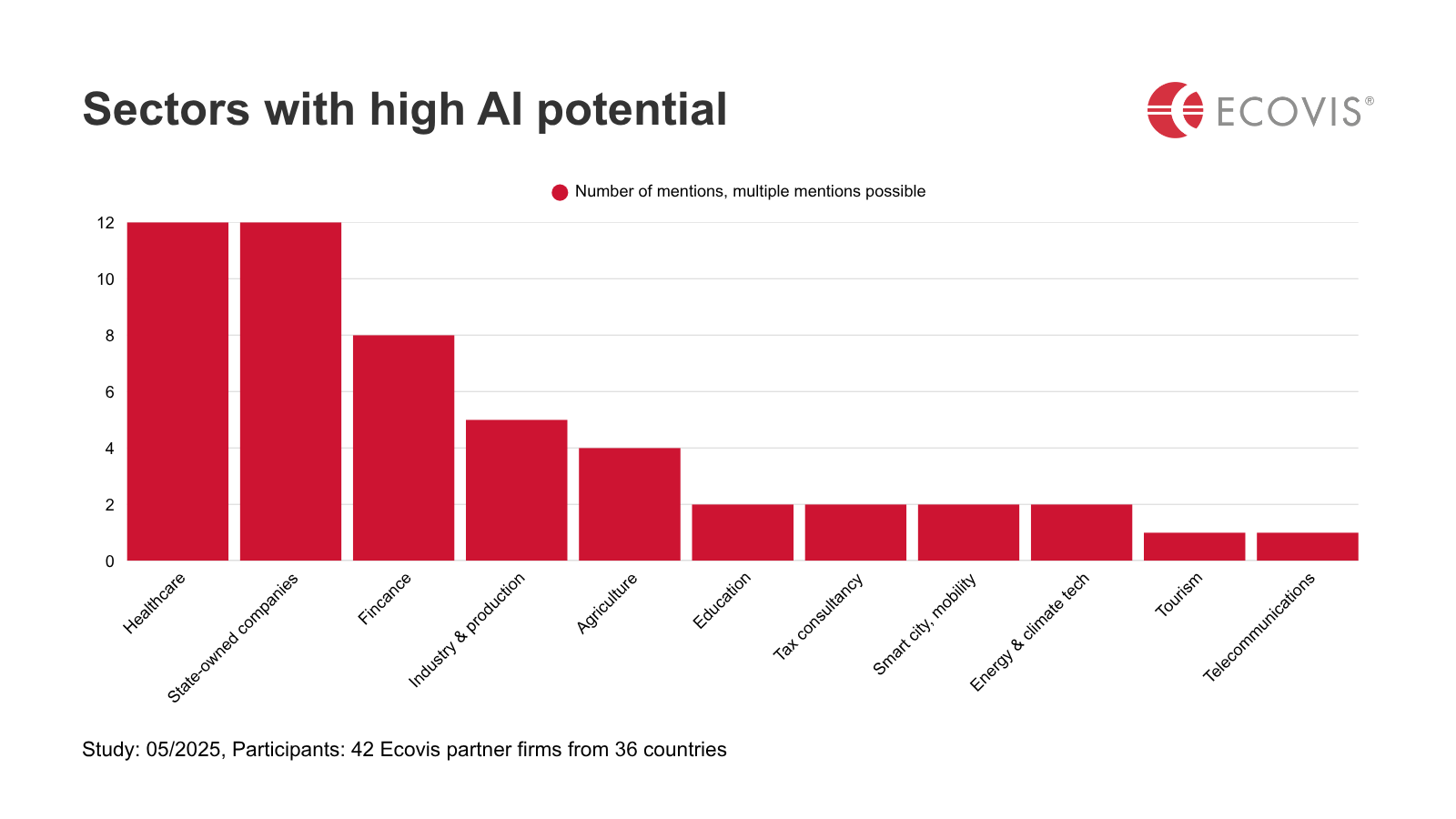

AI potential as a remedy for excessive government bureaucracy?

The sectors with the highest AI potential mentioned in the study are the healthcare sector and government players, as shown in the following chart.

The advantages lie primarily in process automation, increased efficiency, cost reduction and the promotion of innovation and accuracy in work. Many of the 42 participating law firms cite the challenges as legal certainty for companies, personal data protection and strict regulations that prevent innovation.

The responses from study participants show that the potential for improvement lies primarily with government agencies that have high administrative costs. “Agencies and administrations should take advantage of opportunities to streamline their operations and become more efficient”, says Alexander Weigert. “Less overregulation would also please small and medium-sized enterprises, which have to invest too much time in unnecessary bureaucracy. Time that they could use for innovation and productivity.”

Customers from the financial sector are leading the way in AI usage

26 of the partner law firms surveyed stated that their clients are already using AI in the afore-mentioned sectors. Here are a few examples per region:

In the Americas region, Brazil stands out in particular with customer examples: Ecovis financial analyst Celmo Silva states that his customers use AI in the finance sector, retail and the healthcare industry. In all three sectors, the focus is on products and services tailored to the customer. In industry, the main focus is on quality control and maintenance predictions.

In the APAC region, in Taiwan, Malaysia and China AI is primarily used in the financial sector. Ecovis partner Pingwen Hu in China provides an example: thanks to AI fraud detection and robot advisors, risk assessment has become 50 per cent faster. Other areas include telecommunications, skilled trades and commerce.

Within the EU, the financial sector is the most common industry in which Ecovis clients use AI, with five mentions, closely followed by healthcare, retail and the public sector, with four mentions each. Other sectors mentioned include skilled trades, agriculture, legal services and industry. The Portuguese partner Goncalo Areia states, for example, that he has several public companies as clients. Thanks to AI, documents can be exchanged more easily and interaction between citizens and institutions is also made simpler and better. Paris-based lawyer Julien Vaucheret provides a client example from the healthcare sector: costs and time can be saved in preclinical development.

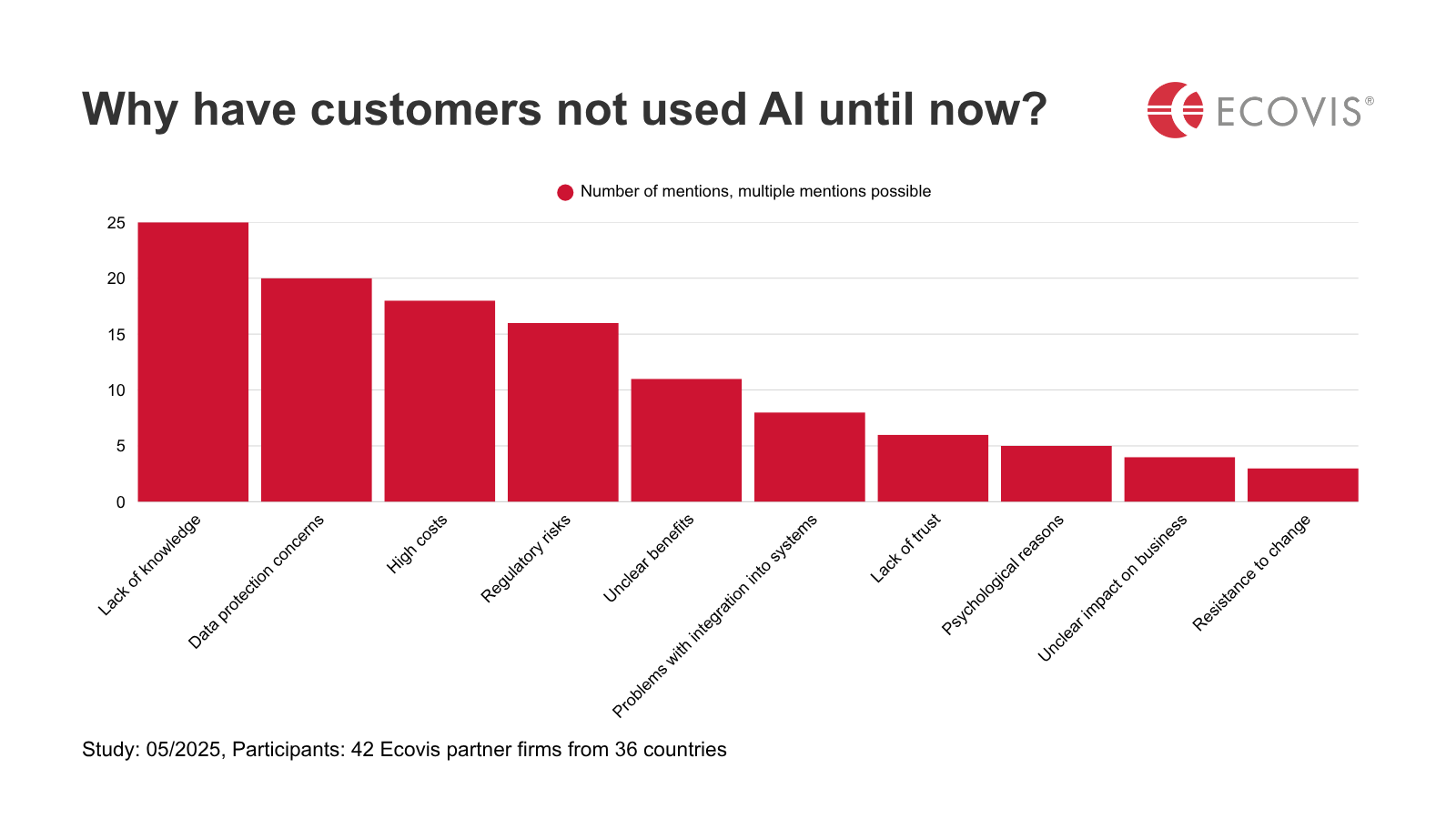

AI usage in companies: lack of knowledge is the problem

The following chart shows the number of responses given by customers as to why they do not yet use AI.

The evaluation shows that technology and data protection also play a role worldwide. However, the biggest obstacles to AI in companies are people: a sometimes massive lack of knowledge about and trust in AI, unclear benefits, psychological reasons such as fear of job losses, and resistance to change.

“This clearly means that anyone who wants to reap the benefits of AI must invest in entrepreneurs and employees,” says Richard Hoffmann. “This can be done, for example, through targeted training in the use of tools and software, with information on data protection rules and, in some cases, discussions to remove uncertainties and break down barriers. Because only those who know for sure what they can and are allowed to do will use AI – especially in sensitive sectors such as healthcare.”

Our assessment: governments must strike a balance

On the one hand, unclear legal requirements; on the other, targeted subsidies – governments worldwide recognise the advantages of AI. However, the question remains: how practical are these innovations in the end if, above all, internationally active companies lack legal clarity regarding their implementation?

“In our view, more cooperation between governments worldwide is needed here. After all, overly strict enforcement or very narrowly worded laws can prevent the potential and opportunities offered by AI from being fully exploited. It is important to find a balance and create a framework for companies that minimises overregulation and bureaucracy while allowing sufficient scope for investment,” says Alexander Weigert. “Our global network includes many experts on AI who monitor current developments and can advise companies on issues relating to legislation and funding.”

Companies should therefore act quickly and familiarise themselves and their employees with the topic of AI and its possible applications. Richard Hoffmann fears that “people’s fears and potentially excessive inconsistent government regulations could mean that AI will continue to receive little support as a valuable complementary tool in many industries.”

About the study

ECOVIS International is an international consultancy network with locations in over 90 countries. Forty-two partner firms from 36 countries participated in the study. The participants were composed as follows by region: eight from South and North America (Americas), seven from the Asia-Pacific region (APAC), 22 from Europe (including 19 EU countries) and five participants from Africa and the Middle East (MEA). The survey consisted of ten questions, three of which were multiple choice and seven open. The survey was voluntary and open for participation for three weeks in May 2025.

Permanent establishment in Germany: New case law on international permanent establishments

08.10.2025

If a foreign company maintains a permanent establishment in Germany, tax obligations may arise. German regulations and double taxation agreements must be taken into account, as well as whether a “permanent establishment” exists. The Ecovis experts explain the latest rulings of the German Federal Fiscal Court (FFC).

A central requirement for the existence of a permanent establishment both under Section 12 of the German Fiscal Code (AO) and under Article 5 of the OECD Model Tax Convention is the “fixed establishment”. This is generally understood to mean premises that are under the legal control of the foreign company (e.g., through lease or ownership or even de facto transfer). The criterion of control is here very important under German law.

The criteria for a permanent establishment in Germany: The rulings of the Federal Fiscal Court

In a recent ruling (I R 47/21, 18 December 2024), the FFC considered permanently restricted usage structures to be an indication of a permanent establishment. The case in question involved a lockable roll container with business documents inside a shared office. This was sufficient to constitute a permanent establishment.

A permanent establishment also requires a certain duration. In another ruling (I R 39/21, 18 December 2024), the FFC addressed the question of how long permanent premises must exist in order to be considered a permanent establishment. Here, the FFC stipulated a minimum period of six months. However, actual business activities must also take place at the premises during this period. If, for example, a lease agreement was concluded for a period of more than six months, but the business activities were already terminated and wound up within six months, there is no permanent premises and therefore no permanent establishment. This view is based on the German understanding of a permanent establishment.

We will clarify with you whether your company has established a permanent establishment in Germany with all the associated tax consequences. Marion Dechant, Accountant, ECOVIS Deutschland, Munich, Germany

What companies in Germany need to consider when setting up permanent establishments

To avoid unintentionally setting up a permanent establishment in Germany with additional tax obligations, particularly in relation to income or corporation tax, companies should be careful with usage structures restricted to specific persons. Even small lockable devices such as cabinets or similar items can constitute a permanent establishment, especially if they are used for business purposes. Also, while the minimum duration of business activities for a permanent establishment provides some planning security, this time requirement should be monitored in practice.

For further information please contact:

Marion Dechant, Steuerberaterin, Ecovis Deutschland, Munich, Germany

Email: marion.dechant@ecovis.com

In the United Kingdom, as of 6 April 2025, a new tax system for the taxation of foreign income and gains (FIG) has applied to individuals who return to the country after a long period of non-residence. It replaces the remittance basis and removes the concept of domicile from UK taxation. The Ecovis advisors explain the details.

Under the FIG regime, individuals who become UK tax residents after ten consecutive years of non-residence, determined by the statutory residence test, are eligible for a four-year exemption from UK tax on qualifying foreign income and gains. Unlike the previous system, there is no requirement to keep funds offshore. Individuals already resident for fewer than four years as of 6 April 2025 may still benefit for the remainder of their initial four-year window.

Those returning to the UK should check carefully to what extent the new FIG rules also apply to them. Josh Mills, Senior Manager Private Client Tax, ECOVIS Wingrave Yeats, London, United Kingdom

Who the new FIG system applies to

Eligibility extends to both those previously considered UK domiciled and non-domiciled, meaning returning UK nationals who were excluded under the remittance basis may now qualify. Claiming the relief under the FIG regime requires foreign income and gains to be declared on the individual’s self-assessment tax return. Taxpayers must make annual claims and specify which sources of income or gains they wish to apply the relief to. It’s important to note that claiming FIG relief results in the loss of both the personal allowance (GBP 12,570) and the capital gains tax exemption (GBP 3,000).

The regime also includes transitional provisions for those who previously used the remittance basis. These include the ability to rebase foreign assets to their 6 April 2017 value and a temporary repatriation facility (TRF), allowing previously ringfenced funds to be remitted to the UK at reduced tax rates, sitting at 12% for the first two years, 15% in the third, and the individual’s marginal rate thereafter.

What other regulations apply?

Other reliefs have been adjusted to align with the FIG regime. Overseas workday relief (OWR) now runs for four years and no longer requires offshore accounts, though it is capped at GBP 300,000 or 30% of qualifying income. Business investment relief (BIR) remains available during the TRF period but will be phased out from April 2028.

Given the complexity and breadth of these changes, individuals affected are strongly encouraged to seek specialist tax advice and conduct a thorough review of their financial affairs.

Good to know: Further information on foreign income and gains

Download our foreign income and gains (FIG) regime factsheet to learn more on how internationally mobile individuals can benefit from tax exemptions and transitional reliefs:

Annual corporate obligations in Spain: Key requirements for companies

06.10.2025

Spanish companies must fulfil a variety of obligations under the Capital Companies Act. The Ecovis consultants explain these in detail.

Spanish companies, whether limited liability (SL) or public limited (SA), are required annually to comply with the legal obligations established by the Capital Companies Act (LSC). These obligations, when managed with expert guidance and supervision, ensure orderly compliance and promote transparency and good corporate governance.

The main annual obligations for companies

Preparation of annual accounts: Directors or administrators must prepare the annual accounts within three months after the end of the financial year. These documents must then be approved by the shareholders’ meeting within the following six months.

Filing with the Commercial Registry: Once approved, the accounts must be filed electronically with the registry within one month (normally before 30 July if the year closes on 31 of December).

Legalisation of corporate books: Companies are required to legalise their corporate books (minutes books, shareholder registers, and accounting records) within four months of the year-end.

Audit obligations: An external audit is mandatory if the company exceeds certain thresholds for assets, turnover, or number of employees. In such cases, auditors must be appointed and registered.

Annual General Meeting (AGM): Companies must hold an AGM to approve accounts, decide on profit distribution, appoint or renew directors, and adopt other relevant resolutions.

Ongoing updates: In addition to the annual cycle, companies must notify the registry of changes such as director appointments, changes of registered office, amendments to bylaws, or powers of attorney.

We provide companies with expert advice on regulatory compliance, allowing them to focus on their growth. Isabel De Ron, Lawyer, Partner, ECOVIS Legal Spain, Madrid, Spain

Advice for companies

Annual obligations can be time-consuming, and delays may lead to penalties or reputational risks. Early planning and the support of legal professionals ensure that all requirements are handled properly, and nothing is left to chance. Companies should ensure that their advisors can support them in preparing and filing annual financial statements, convening and documenting shareholder and board meetings, or certifying company books and processing electronic filings.

Natural Catastrophes in 2025: Record Global Losses and Growing Climate Risk

02.10.2025

The first half of 2025 has proven to be among the costliest ever in terms of economic losses caused by extreme events. According to the latest report published by Swiss Re Institute, total losses reached 143 billion US dollars, of which 135 billion were the result of natural catastrophes and 8 billion from man-made events. This figure is well above the ten-year average of around 106 billion dollars and confirms an ongoing trend of rising costs linked to natural disasters, with annual growth estimated between 5 and 7 percent.

Equally significant is the level of insured losses, which rose to 80 billion dollars, almost double the ten-year average of 47 billion. On the one hand, this indicates a broader diffusion of insurance coverage, which today compensates around 56 percent of total economic damages. On the other hand, it highlights the growing pressure on the insurance industry, which is being forced to cope with increasingly severe risks and events that often present extraordinary characteristics.

The semester was marked in particular by the wildfires in California, which alone caused around 40 billion dollars in damages an unprecedented figure for a single event of this kind. Weather conditions, characterized by prolonged and intense Santa Ana winds, fuelled the rapid spread of the flames, making the emergency particularly devastating. In addition to these fires, the United States was hit by a series of severe thunderstorms, responsible for further substantial losses and marked by high volatility that makes forecasting and preventive planning extremely difficult.

The picture was different in Europe and Italy, where the first six months of the year passed with low levels of extreme events and without any episodes comparable to those observed across the Atlantic. However, Swiss Re analysts point out that historically the second half of the year accounts for about 60 percent of insured losses from natural catastrophes, largely due to the Atlantic hurricane season and the intensification of extreme weather phenomena during the summer and autumn. As a result, the outlook remains highly uncertain, and there is a strong possibility that 2025 could close with losses exceeding initial projections.

The report once again underlines how climate change, the expansion of urbanization into vulnerable areas, and the rising value of exposed assets are transforming natural catastrophes from exceptional events into structural drivers of global risk. For businesses, investors, and the insurance sector, this means the need to increasingly integrate climate risk management into their strategies and prepare for growing volatility. The first half of 2025 therefore represents yet another wake up call, and the second half of the year will be decisive in determining whether we are facing a new all time record for global losses.

ATO Tax Changes: Four Developments To Watch 2025/26

26.09.2025

Taxpayers are navigating a shifting landscape this financial year as the Australian Tax Office tightens its approach, and new reforms and legal challenges gather momentum. The Ecovis experts from ECOVIS Clark Jacobs outline four matters to keep on the radar.

No More Deduction for ATO Interest

From 1 July 2025, interest on overdue tax debts (the ATO General Interest Charge) is no longer deductible. This change follows concerns about the ATO’s rising debt book, which now exceeds $100 billion, and is designed to discourage taxpayers from using the ATO as a de facto bank by stretching out payments.

ATO Intensifies Debt Collection

The ATO is stepping up debt collection efforts. Garnishee notices, credit reporting referrals and director penalty notices are becoming more common, and we expect this trend to continue. Businesses and individuals will need to monitor their tax obligations more carefully and plan ahead to avoid additional costs.

Proposed Higher Tax for Superannuation Balances Above $3 Million

The government’s plan to impose higher taxes on superannuation balances above $3 million remains on the agenda. A major point of contention is the inclusion of unrealised gains, which challenges the long-established principle of only taxing realised income and capital gains. While compromises may still be made, some form of this measure is likely to pass into law.

For individuals with significant superannuation holdings, particularly those with property or other appreciating assets in their fund, this could have real implications for future planning. The threshold also isn’t indexed, which means more Australians may be affected over time as asset values increase.

Childcare Costs and Deductibility

A law firm has recently applied for ATO funding to revisit a 1972 High Court ruling that deemed childcare costs a private expense, and therefore non-deductible. More than 50 years on, the context has shifted significantly: childcare is often essential for parents to participate in the workforce and increase their taxable income.

If this challenge gains traction and the government ultimately legislates a change, the way childcare support is provided could look very different. A tax deduction managed through the ATO could potentially replace or simplify the current subsidy system, making life easier for many families.

Final Thoughts

The 2025/26 financial year is already shaping up as challenging for many taxpayers, with the ATO taking a harder line on debt collection and deductions. At the same time, proposed reforms to superannuation and the renewed debate on childcare costs suggest further changes are ahead. Staying informed and proactive will be critical for both individuals and businesses, to help minimise exposure to unexpected costs and provide greater certainty in tax and financial planning.

Paying in Vietnam: Government calls for greater promotion of cashless payments

24.09.2025

Vietnam is promoting cashless payments. The relevant authorities must therefore implement measures to promote cashless transactions, improve governance and advisory services, and conduct comprehensive communication campaigns. The Ecovis experts explain the details.

According to the Prime Minister’s official circular 124/CD-TTg of 30 July 2025, the Ministry of Finance is responsible for coordinating with other ministries and sectors to tighten inspections and oversight of state budget disbursement. It must also ensure compliance with legal regulations on invoices and payment documentation relating to the sale and purchase of goods and services. Violations, particularly the deliberate use of cash to evade taxes, must be promptly and strictly penalised.

The role of the State Bank in the further development of cashless transactions

The State Bank of Vietnam (SBV) will work with the relevant agencies to quickly implement solutions to further develop the cashless payment ecosystem. It has also been assigned to conduct a comprehensive review of the implementation of the 2021-2025 cashless payment development scheme and present its results to the Prime Minister before 1 December 2025.

In addition, the SBV must step up inspection, supervision, and anti-money laundering measures within the banking system. The continued development of payment infrastructure and financial technologies is also seen as essential to boosting cashless transactions nationwide.

According to a recent SBV report on cashless payment in Vietnam, the interbank electronic payment system currently processes an average of VND 820 trillion (USD 31.25 billion) daily, handling around 26 million transactions.

The Vietnamese government is promoting cashless payments to make payments easier and prevent tax evasion. Trung Pham, Partner, ECOVIS AFA VIETNAM, Da Nang City, Vietnam

Cashless transactions are increasing steadily

Vietnam has continuously upgraded its national credit information infrastructure, achieving an impressive 98 percent data update success rate across credit institutions. There are now over 204.5 million payment accounts and 154.1 million active bank cards in the country, with nearly 87 percent of adults holding bank accounts. A recent survey revealed that 59 percent of daily transactions are cashless, rising to 72 percent among those aged 25 to 44.

Vietnam is also advancing cross-border retail payments via QR codes with neighbouring countries such as Thailand, Laos, and Cambodia, with plans to expand further across Asia. Previously, in Article 26 of Decree No. 181/2025/ND-CP, effective from 1 July 2025 detailing the implementation of a number of articles of the Law on Value Added Tax, the government also stipulated: “Business establishments must have non-cash payment documents for purchased goods and services (including imported goods) of VND 5 million or more, including value added tax”. Under the previous regulation, this threshold was VND 20 million or more, inclusive of value added tax.

This underlines the government’s commitment to non-cash payments in production and business activities, which is expected to help tax authorities manage more effectively, reduce budget losses, and make large-value transactions more transparent.